Contribution Margin: What It Is, How to Calculate It, and Why You Need It

Given the described circumstances, this contract would be recognized in the same period regardless of whether it was classified as an exchange or contribution. In addition, the determination of the fair value of publicity is highly subjective. Thus, any allocation between exchange and contribution revenue would provide little benefit. FASB has recently released new guidance on how to determine whether a transaction is a contribution or an exchange. The authors explain how the new guidance works and provide examples of how nonprofits should apply it when recognizing revenue from these transactions. Regardless of how contribution margin is expressed, it provides critical information for managers.

Submit to get your question answered.

- Charlie, however, receives more than positive sentiment, such as greater visibility than Bravo and the means to promote itself and its products.

- Recipients need to understand the terms of each of their contribution agreements, because none of the indicators listed above definitively distinguish a contribution from an exchange.

- The break-even point, or BEP, is the point at which the cost incurred and the revenues generated are equal.

- ABC Foundation would thus apply Topic 606 in accounting for this transaction.

- Investors examine contribution margins to determine if a company is using its revenue effectively.

In our example, if the students sold \(100\) shirts, assuming an individual variable cost per shirt of \(\$10\), the total variable costs would be \(\$1,000\) (\(100 × \$10\)). If they sold \(250\) shirts, again assuming an individual variable cost per shirt of \(\$10\), then the total variable costs would \(\$2,500 (250 × \$10)\). The contribution margin is the foundation for break-even analysis used in the overall cost and sales price planning for products.

Contribution Margin: What It Is, How to Calculate It, and Why You Need It

These materials were downloaded from PwC's Viewpoint (viewpoint.pwc.com) under license. Contributions made shall be measured at the fair values of the assets given or, if made in the form of a settlement or cancellation of a donee’s liabilities, at the fair value of the liabilities cancelled. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals.

What is a good contribution margin?

This highlights the margin and helps illustrate where a company’s expenses. Variable expenses can be compared year over year to establish a trend and show how profits are affected. Based on the contribution margin formula, there are two ways for a company to increase its contribution margins; They can find ways to increase revenues, or they can reduce their variable costs. On the other hand, variable costs are costs that depend on the amount of goods and services a business produces. The more it produces in a given month, the more raw materials it requires.

Do you already work with a financial advisor?

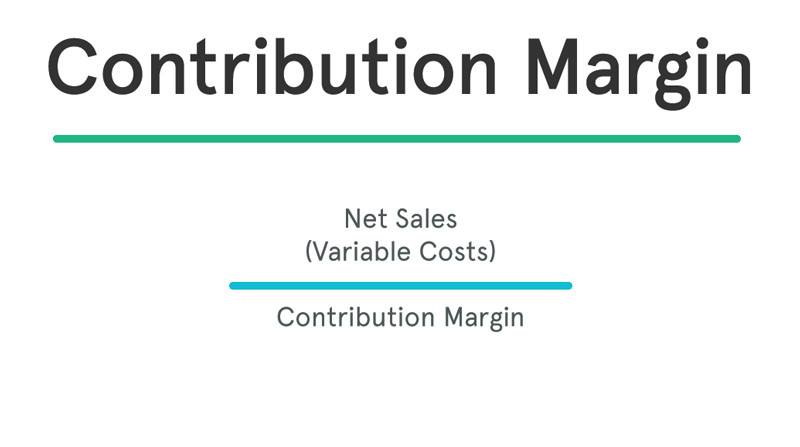

If the company’s contribution margin ratio is higher than the basis for comparison, the result is favorable. The contribution margin subtracts the variable costs for producing a single product from revenue. The contribution margin measures the profitability of individual items that a company makes and sells. This margin reviews the variable costs included in the production cost and a per-item profit metric, whereas gross margin is a company's total profit metric. Direct production costs are the cost of goods sold (COGS) and include raw materials, labor, and overhead attributed to each product. The gross margin shows how well a company generates revenue from direct costs such as direct labor and direct materials costs.

Fixed costs are production costs that remain the same as production efforts increase. A key characteristic of the contribution margin is that it remains fixed on a per unit basis irrespective contribution definition in accounting of the number of units manufactured or sold. On the other hand, the net profit per unit may increase/decrease non-linearly with the number of units sold as it includes the fixed costs.

Contribution margin may also be expressed as a ratio, showing the percentage of sales that is available to pay fixed costs. A business can increase its Contribution Margin Ratio by reducing the cost of goods sold, increasing the selling price of products, or finding ways to reduce fixed costs. In the United States, similar labor-saving processes have been developed, such as the ability to order groceries or fast food online and have it ready when the customer arrives. Do these labor-saving processes change the cost structure for the company? It is important to note that this unit contribution margin can be calculated either in dollars or as a percentage.

Yes, the contribution margin will be equal to or higher than the gross margin because the gross margin includes fixed overhead costs. The contribution margin excludes fixed costs, so the expenses to calculate the contribution margin will likely always be less than the gross margin. Contribution margin is not an all-encompassing measure of a company's profitability. However, contribution margin can be used to examine variable production costs. The contribution margin can also be used to evaluate the profitability of an item and calculate how to improve its profitability, either by reducing variable production costs or increasing the item's price.

Using this contribution margin format makes it easy to see the impact of changing sales volume on operating income. Fixed costs remained unchanged; however, as more units are produced and sold, more of the per-unit sales price is available to contribute to the company’s net income. The contribution margin income statement separates the fixed and variables costs on the face of the income statement.

প্রকাশক : মাসুদ রানা সুইট । সম্পাদক : আবুল হাসনাত অমি । নগর সম্পাদক : ইফতেখার আলম বিশাল নির্বাহী সম্পাদক : রুবেল আহম্মেদ । মফস্বল সম্পাদক : মোস্তাফিজুর রহমান । ব্যবস্থাপনা সম্পাদক : নীলা সুলতানা । বার্তা সম্পাদক : -------------- । সহ-বার্তা সম্পাদক : আলিফ বিন রেজা । সহ-বার্তা সম্পাদক :

Copyright © 2024 Dainiksopnerbangladesh.com. All rights reserved.